Posted by Dave Kaplan

5 years ago / June 22, 2021

The 2021 Cannabis Vape Retailer Product Hot List

Despite the emergence of COVID-19, the US cannabis vape industry had its best year on record in 2020 with just over $2b in sales. Those who wrote off the sector’s sales boom as an outlier have quickly been proven wrong in 2021, where sales have already surpassed the $1b mark through May.

The vape category is absolutely trending in the right direction, its rampant sales fueled by simultaneous advancements in extraction technology, hardware, and product quality. More vape products are being moved now than ever before. But not all products are equal in consumers’ eyes, according to the data. Like in any industry, some vape product types are driving sales. Others have fallen to the wayside.

With Q3 set to kick off in a couple of weeks, and retailers around the US currently mulling over which products to stock their shelves with during the second-half of the year, we thought it would be prudent to look at two vape product types currently in high demand and a couple that are not.

As always, we couldn’t present this retail POS data to you without help from our friends at Headset Insights, whose cannabis vape data platform is, without a doubt, the most comprehensive in the industry. We hope this information helps your business finish 2021 strong. For a complete breakdown of cannabis vape sales by US and Canadian markets, make sure to also download our free quarterly cannabis vape report, published recently in partnership with The Arcview Group and Headset.

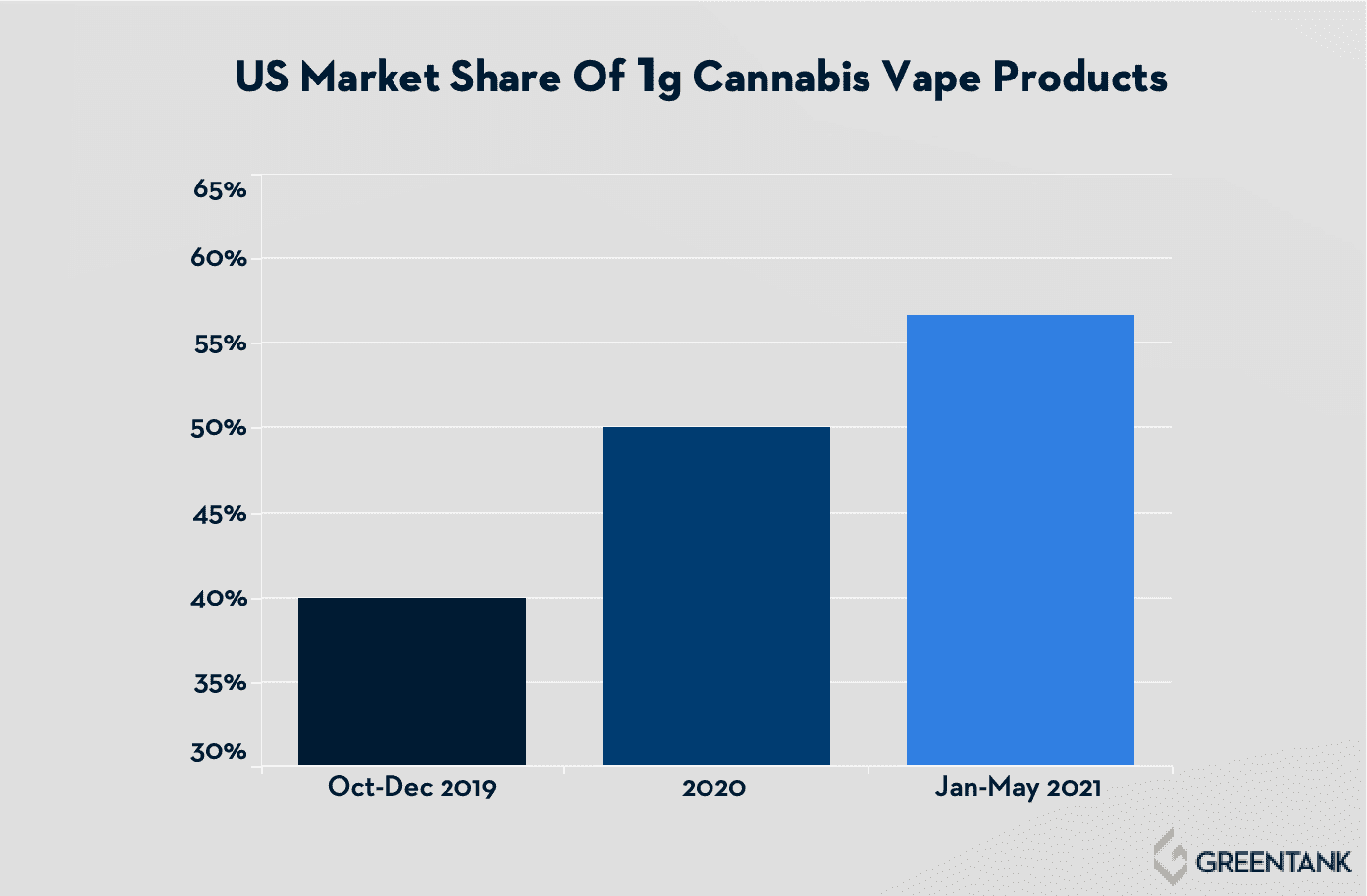

Hot: 1g Cartridges

Consumer demand for 1g cartridges has been steadily on the rise in the US since 2018. By the end of 2019, 1g units accounted for over 40% of all vape products sold across California, Colorado, Nevada, Washington, and Oregon. That number increased to over 50% of the vape market by Q4 2020, and currently stands at 56.6% of all units sold through the first five months of 2021.

In some of the nation’s older and more entrenched markets, the sale of 1g cartridges is currently dominating all other unit sizes. In Washington, 1g units account for 88% of all units sold. In Oregon, they make up 90.2% of vape sales. Even in Colorado, where 0.5g vape products traditionally reign, the popularity of 1g cartridges has doubled over the last 12 months to 40% of all vape products sold!

We suspect that value and quantity are the two primary factors driving consumers to this unit size, although the potential reduced waste that a larger cartridge size offers likely also appeals to environmentally-conscious user demographics. Whatever consumer motivations may truly be, 1g units are a hot-ticket item at the moment, and will likely only become more popular going forward.

Hot: Live Resin Products

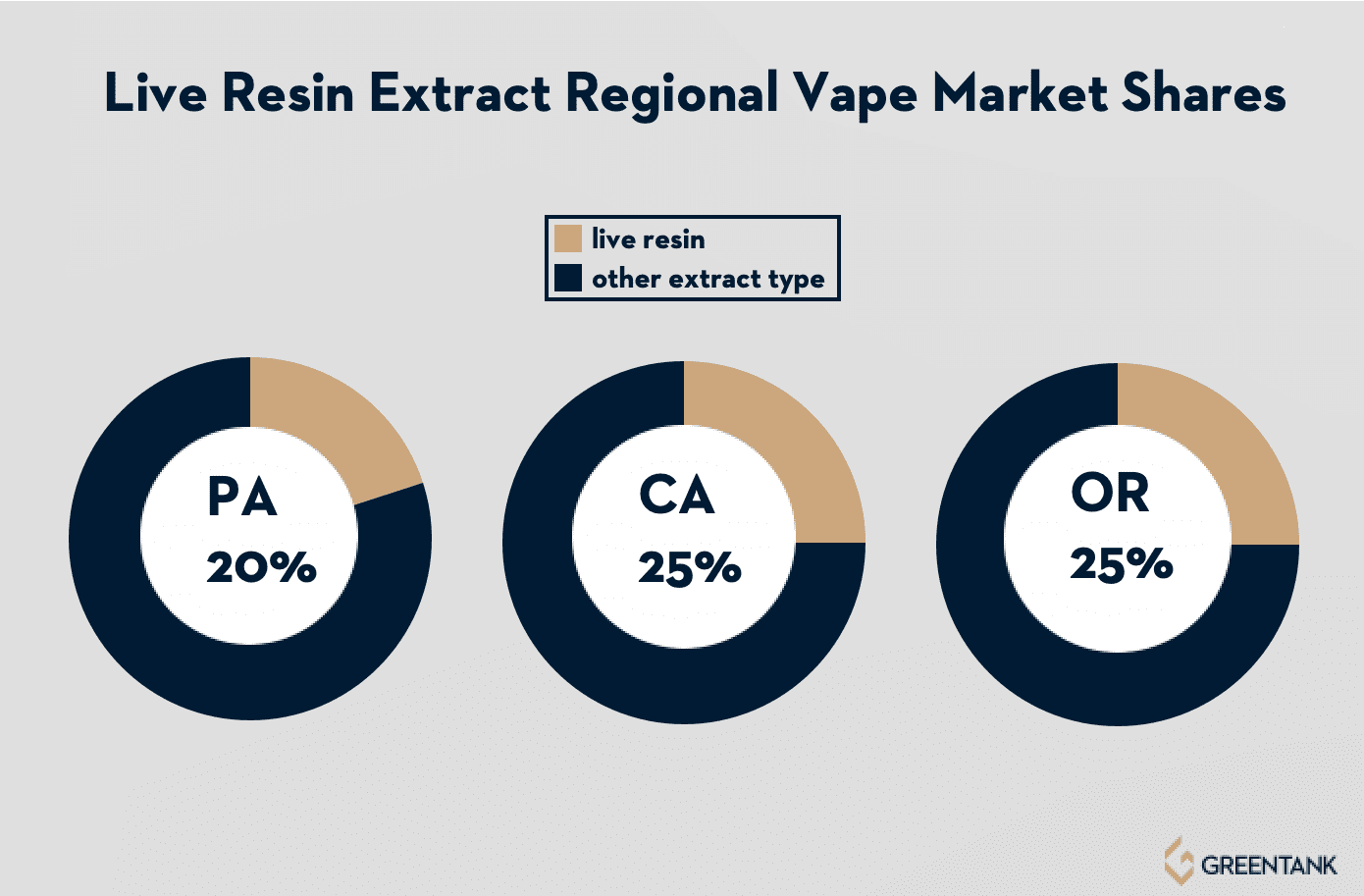

Last year, we wrote about the rising popularity of live resin extracts. Flash-frozen directly after harvest and then extracted to retain more terpenes, these immensely flavorful, aromatic, and potent vape products are taking the industry by storm.

The market share of live resin products within the US vape sector has never been higher. In fact, it’s nearly tripled to 20.7% since November 2019. This metric can be seen first-hand in Pennsylvania, where 1 out of every 5 vape products currently sold is a live resin extract, or in California and Oregon, where live resin extracts now account for 1/4 of all cannabis vape sales!

The segment’s monthly sales growth is even more impressive. Through the first five months of 2021, live resin vape sales in the US are on pace to nearly double their 2020 total of $329.9M. The majority of that revenue comes from California, where live resin vape products have generated an average of $23.7M in sales each month this year. But the popularity of the extract type is also up across the board in each of CO, WA, OR, NV and PA over the last 18 months, with no indication that this trend will be slowing down or reversing course anytime soon.

Not Hot: CBD Vape Products

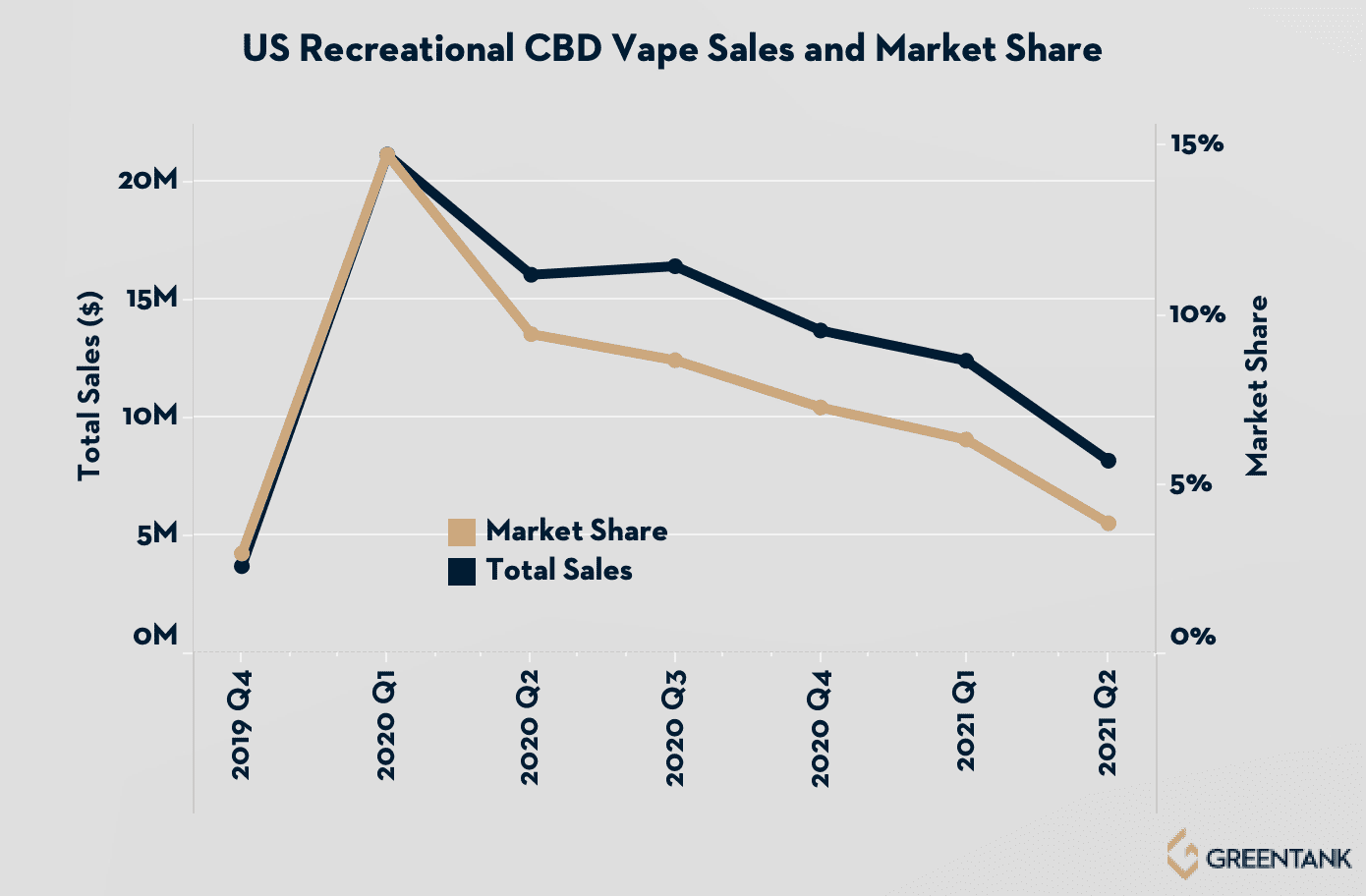

When the Farm Bill passed in December 2018, there was an abundance of optimism in the vape sector about CBD vape products. The mainstream fascination with the cannabinoid, coupled with the fastest-growing delivery method category in the cannabis industry, seemed like it would be a home run with consumers. But, for whatever reasons, the popularity of CBD vape products has not yet taken off in rec-legal states across the US.

After peaking in Q1 2020 with $21M in revenue, the sale of CBD vape products in rec-legal US states has steadily declined. Average monthly sales of the product category dropped to $5.2M the following quarter and then tumbled to $4.4M in Q4. Through the first five months of 2021, CBD vape products have sold, on average, $4M per month nationally and account for only 2% of the overall cannabis vape market! Approximately half of those sales come from California. In Nevada and Oregon, CBD vape sales are practically non-existent, having brought in paltry totals of $636K and $1.1M, respectively, over the last three months.

The jury’s still out on why CBD vape products haven’t caught on among consumers with the same fervor as THC. One possible explanation is that CBD’s wellness-seeking demographics are less drawn to inhalable delivery systems as they are to topical and sublingual applications. Another is that many vape hardware manufacturers haven’t adjusted their product lines to handle the nuances of CBD extracts optimally, which has led to underwhelming user experiences with these products.

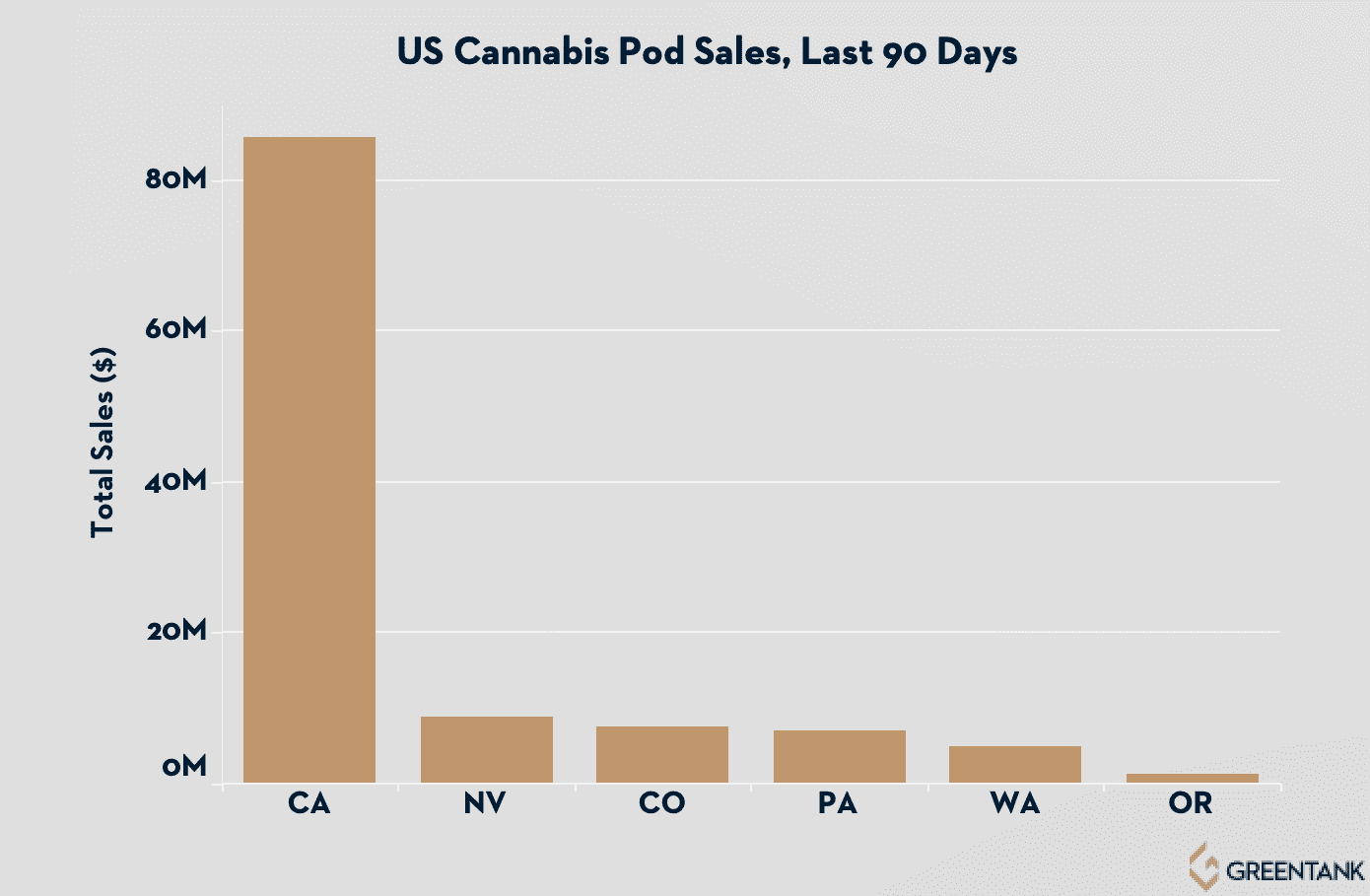

Not Hot: Pod Products That Aren’t STIIIZY

Over the last 90 days, pod cannabis vape products have generated $111.9M in sales across rec-legal markets in the US—roughly 18% of all vape sales in these markets over this time period. Numbers, however, can often be deceiving.

California-based STIIIZY, the top-selling cannabis vape brand in the world, currently dominates the pod segment with 57.8% of its sales. Over the last 90 days, that has amounted to $64.7M, primarily in California. PAX pods are second in this category with 15.63% of the pod market, or 2.8% of the entire vape market. But the $16.6M in sales that PAX pods have generated over the last three months is a significant drop off from STIIIZY, given that they are available for purchase in each of the six markets we track. The numbers only get less encouraging from there. In fact, over the last 90 days, the combined sales from the other eight cannabis pod manufacturers Headset tracks only account for 4.8% of the outright vape market.

While pod products sell like hotcakes in California ($85.6M over the last three months, thanks mainly to STIIIZY), they don’t perform nearly as well in other markets. In Colorado, Nevada and Pennsylvania, the sale of cannabis pods has averaged between $2.5 – $3M per month over the last 90 days. During the same time in the Pacific Northwest, the sale of pods has nearly evaporated: In Washington, pods generated an average of $1.6M in sales over the last three months and in Oregon, they didn’t even bring in an average of $500K a month.

The Bottom Line

To be clear, we’re not saying that CBD extracts or pods are inferior vape products. We’ve tried many that are exceptional! Nor are we advocating that consumers should steer clear of them, either. We are simply pointing out that these product types are currently not popular among cannabis vape user demographics.

Both categories could experience sales spikes in the future. We suspect that CBD extracts will eventually rise in popularity as more hardware manufacturers gain a better understanding of the nuanced and manifold ways the extract interacts with heating elements and other hardware components. Until those tides turn, however, we highly recommend that retailers go with what is currently selling best.

To learn more about what specifically is trending in the vape market where your business operates, reach out to Greentank today. Our market matching consultations are free because we want our partners to succeed and believe that forming a cohesive, data-driven approach at the onset of any hardware consultation puts them in the best position to do so. That’s the difference between a hardware partner and a hardware vendor.

Filed Under:

Tagged with:

![]()

![]()

Join our awesome community

Keep up to date on all Greentank Technology news and promotions

Interested in our products?

Contact us to find out how you can carry the most reliable vape hardware solutions on the market.

General Requests

Logistics