Posted by Dave Kaplan

4 years ago / August 6, 2020

The Greentank U.S. Cannabis Vape Market Report: COVID-19 Edition

COVID-19 has affected the cannabis industry in myriad ways. It forced some legal markets to go on temporary hiatuses, caused others to thrive, and changed the ways cannabis companies operate and consumers purchase their cannabis. These modifications to the cannabis industry have been written about in great detail over the last few months, but very little has been published on the subject of how COVID-19 has affected the cannabis vape market, specifically.

Until now.

To get the most comprehensive picture of how COVID-19 has affected the U.S. cannabis vape market, we delved into the data ourselves using BDSA’s GreenEdge analytics platform. Our strategy was to compare snapshots of both the overall industry and its individual markets from January-May 2019 and January-May 2020, and the results were fascinating. Not only did we discover that the vape market is on pace to exceed last year’s totals, it’s also changed significantly over the last 18 months in terms of product popularity! Let’s take a closer look at some of our findings.

The Overall U.S. Vape Market

While COVID-19 has reduced vape sales in some major markets, the effect hasn’t been nearly as detrimental as you might believe. In fact, due to the emergence of new recreational markets, such as Illinois, Michigan and Massachusetts, and booming medical markets, including Arizona and Maryland, the cannabis vape sector is set to have its strongest year yet.

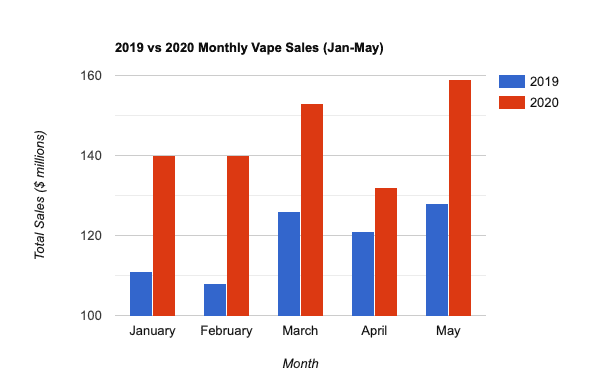

From January-May 2019, BDSA tracked a total of 18 million vape units sold in the U.S. market, resulting in gross sales of $678 million for those five months. Sales in January-May 2020, however, increased to $817 million with 22 million total units sold! The data also shows that each month’s total cartridge sales increased from a year ago and that disposable sales for the five-month period were up 30% from 2019.

Cannabis Vape Market Breakdown

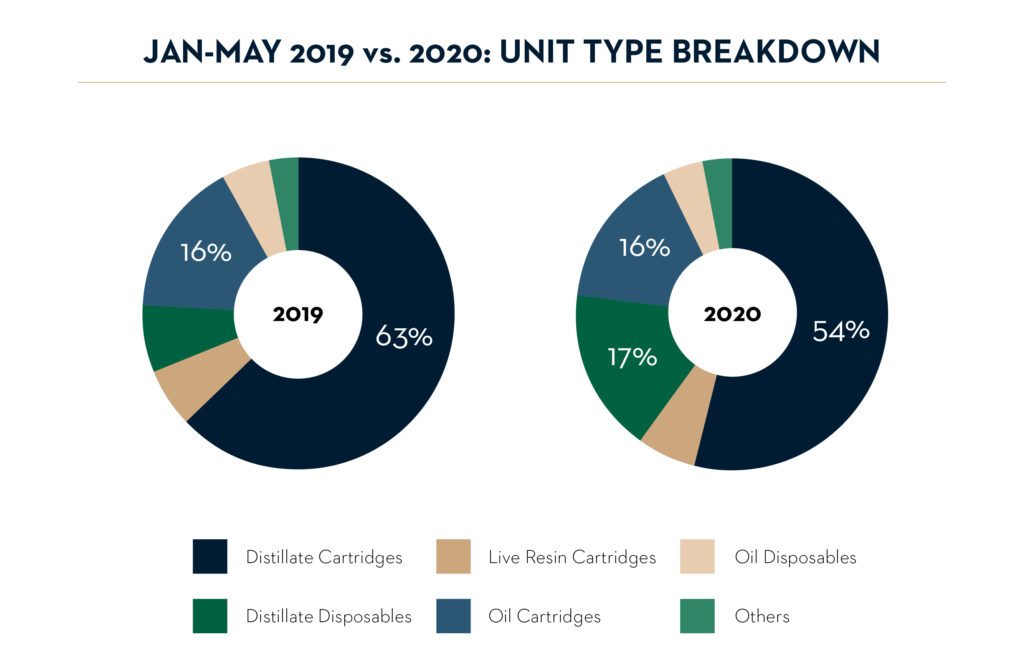

A few noticeable shifts have taken place in the vape space over the last 18 months. Let’s start with live resin cartridges, which have emerged as a new prominent subcategory in 2020.

In Jan-May 2019, distillate cartridges accounted for 63% of total vape product sales. At the time, live resin cartridges were just starting to make an appearance in a few U.S. markets and only garnered 7% of the vape market share with $49 million total in sales. Between Jan-May 2020, however, live resin cartridges spiked to 17% of the vape market share, amassing $142 million in sales—an increase of 241% from the same time period last year. Although nearly indistinguishable in the graphs above, live resin disposables also increased significantly during this time from $1 million in total sales over the first five months of 2019 to $6 million over the first five months of 2020.

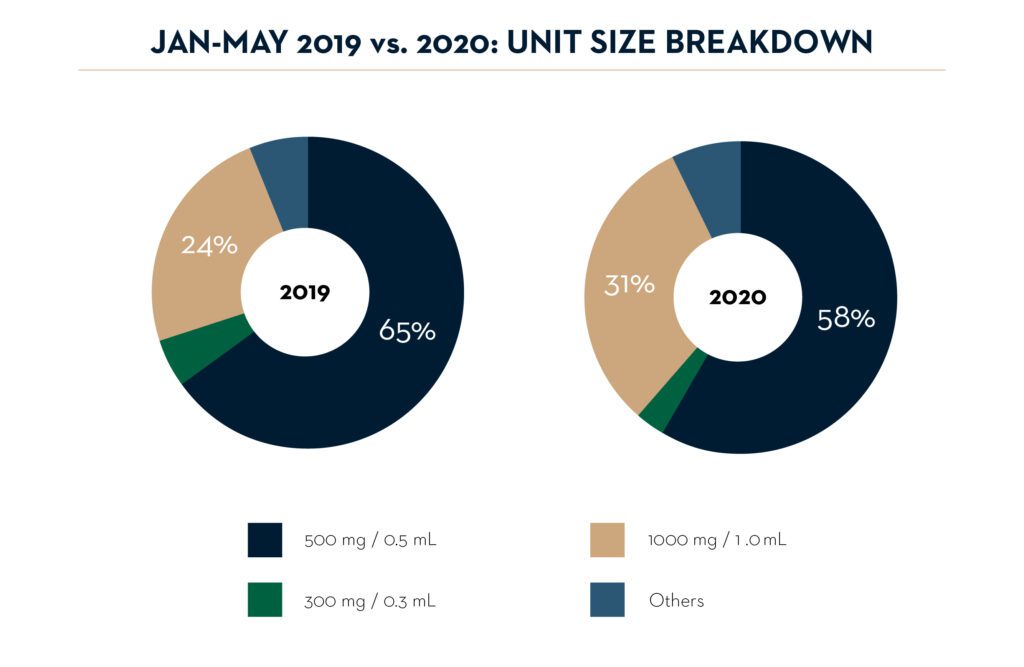

The data also shows that the industry is making a move toward 1000mg (1.0g) cartridges, pods and disposables. Between Jan-May 2019, 1000mg units accounted for 24% of total vape sales with 4.39 million units sold, while 500mg (0.5g) units dominated the market with 65% of total sales. In the first five months of 2020, however, 1000mg units spiked to 31% of total vape sales with over 7 million units sold. During this time, 500mg units dropped to 58% of the total market! It will be interesting to observe whether this trend continues over the next 12 months.

Individual U.S. Markets

California:

Colorado:

Oregon:

Nevada:

Illinois:

Massachusetts:

Maryland:

Arizona:

Filed Under:

![]()

![]()

Join our awesome community

Keep up to date on all Greentank Technology news and promotions

Interested in our products?

Contact us to find out how you can carry the most reliable vape hardware solutions on the market.

General Requests

Logistics